The Argument for Diversification

For as long as I can remember, the asset management industry has been pushing and promoting diversification. Investors have been brainwashed into thinking that responsible investing requires diversification. I believe just the opposite is true, too much diversification is actually irresponsible and only assures average (or below average) performance and higher brokerage fees, both negatives for investors. The financial industry loves to sing the diversification mantra, but you should avoid being over-diversified.

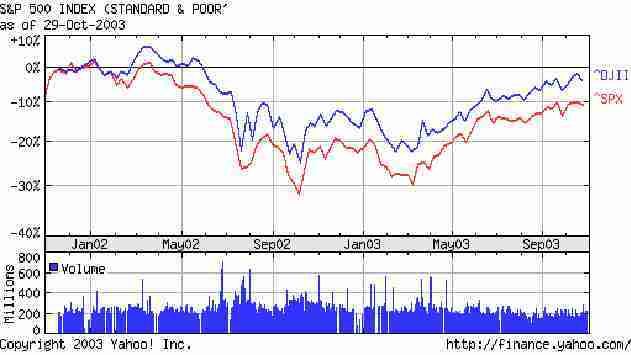

Chart 1: Dow 30 Stocks vs. S&P 500 Index

This two-year chart of the Dow Jones (top line) versus the S&P 500 Index shows that a portfolio of 30 stocks is as diversified as a portfolio of 500 stocks. In fact many studies show that 15 stocks yield the same diversification benefits.

You hear so much about diversification for the following two reasons. First, if you construct a portfolio of numerous companies, a problem or temporary business downturn at any one company will not ruin your return. This is logical because of the law of averages, while something goes wrong at one company, something will likely be going right at another. The other companies in the portfolio will take up the slack until the poor performer improves. The second, and more insidious, reason diversification is so hyped, is that it acts as a safety net and a fee generator for brokerage firms. If a broker recommends 50 stocks or 10 mutual funds to you, the likelihood that you will experience extremely adverse returns is so low that brokers don’t have to worry about stock selection, they just have to worry about getting you to own enough stocks (or funds). The best part of all this diversification nonsense is that it did not help investors at all during the 2000 – 2003 time period when so many investors suffered extreme losses from the Internet bubble. By pushing so many stocks and funds, brokerage firms have essentially guaranteed hefty fee income. The longer investors believe in the diversification story, the more fees will roll in. When I was first developing the groundwork for the Perpetual Value Fund in 1997, I immediately realized that the industry was not promoting rational diversification, they were promoting over-diversification.

Mutual Funds Wear Halloween Costumes Year-round

Everyday is Halloween for the mutual fund industry. Why? Because funds that are supposed to be actively managed are really just index funds dressed-up as actively managed funds. I would really have no problem with this except you pay 2% - 3% (including all fees) to own an actively managed mutual fund, versus 1/2% to own an index fund (where a fund manager only has to mimic an index, no decision making is required). Mutual funds are so diversified, you would be better off just buying an index fund. Most fund managers have too many stocks in their portfolios, anywhere from 50 to 200 or so. Look at the chart on page one of the Dow Jones Industrial Average versus the S&P 500 Index over the past two years. The lines are nearly identical, yet the Dow only has 30 stocks and the S&P has 500 – adding the additional 470 stocks to a portfolio would have actually hurt the performance.

What Really Happens when you Diversify

Though I picked two years for the chart on page one, almost any timeframe would show the Dow 30 outperforming the S&P 500 Index (even if just slightly). The reason this happens is that the Dow is comprised of the 30 highest quality industrial companies that represent (theoretically) the entire market. By limiting the index to 30 names, the Dow generally represents quality capital allocation opportunities. Compare this to the S&P 500, which does the same thing as the Dow, only it uses 500 companies. Clearly, if you have to make 500 capital allocation decisions, each successive decision will be worse than the prior decision.

That is the problem with over-diversification, every additional asset allocation decision you make is by definition weaker than the previous investment. So what are you left with when you over-diversify? At best average performance, and at worst massive under performance due to the excessive fees you incur buying and selling so many stocks (or funds).

Your performance will be average at best, because you have essentially diversified away all your hard work and research. You have watered your portfolio down with lower quality stocks. You are left with stock market risk not company specific risk, just the opposite of what you want. If the market goes down, your 30 companies will go down, if the market goes up, your 30 companies will go up. By over-diversifying you are leaving your portfolio at the mercy of the markets. Most financial professionals would have you believe this is a wise decision, I am telling you it is not.

Why do all the Research if you are Going to Diversify

As many of you know, I do not believe in a diversified portfolio. At Perpetual Value I can hold a maximum of ten positions, and I have no problem owning as few as four companies. I think the fund’s concentrated portfolio is its biggest selling point. Most investors simply do not have access to a similar product. You may be able to go to a broker and structure a concentrated portfolio, but you can rest assured the broker’s fee will not be contingent on whether or not you make money. The broker gets paid either way. In addition, any mutual fund you buy will have considerably more than 10 positions. The Perpetual Value fund is unique in that I am not scared to run a concentrated portfolio.

I believe that the whole point of portfolio management is to identify above average companies in which to invest. Finding such companies at reasonable prices is nearly impossible. It happens a handful of times a year if we are lucky. That is why the fund is so inactive, patience is a key component of our investment discipline.

Over-diversification is yet another way the financial industry has failed the investing public. It is far better to buy a handful of quality companies than many mediocre companies.

For as long as I can remember, the asset management industry has been pushing and promoting diversification. Investors have been brainwashed into thinking that responsible investing requires diversification. I believe just the opposite is true, too much diversification is actually irresponsible and only assures average (or below average) performance and higher brokerage fees, both negatives for investors. The financial industry loves to sing the diversification mantra, but you should avoid being over-diversified.

Chart 1: Dow 30 Stocks vs. S&P 500 Index

This two-year chart of the Dow Jones (top line) versus the S&P 500 Index shows that a portfolio of 30 stocks is as diversified as a portfolio of 500 stocks. In fact many studies show that 15 stocks yield the same diversification benefits.

You hear so much about diversification for the following two reasons. First, if you construct a portfolio of numerous companies, a problem or temporary business downturn at any one company will not ruin your return. This is logical because of the law of averages, while something goes wrong at one company, something will likely be going right at another. The other companies in the portfolio will take up the slack until the poor performer improves. The second, and more insidious, reason diversification is so hyped, is that it acts as a safety net and a fee generator for brokerage firms. If a broker recommends 50 stocks or 10 mutual funds to you, the likelihood that you will experience extremely adverse returns is so low that brokers don’t have to worry about stock selection, they just have to worry about getting you to own enough stocks (or funds). The best part of all this diversification nonsense is that it did not help investors at all during the 2000 – 2003 time period when so many investors suffered extreme losses from the Internet bubble. By pushing so many stocks and funds, brokerage firms have essentially guaranteed hefty fee income. The longer investors believe in the diversification story, the more fees will roll in. When I was first developing the groundwork for the Perpetual Value Fund in 1997, I immediately realized that the industry was not promoting rational diversification, they were promoting over-diversification.

Mutual Funds Wear Halloween Costumes Year-round

Everyday is Halloween for the mutual fund industry. Why? Because funds that are supposed to be actively managed are really just index funds dressed-up as actively managed funds. I would really have no problem with this except you pay 2% - 3% (including all fees) to own an actively managed mutual fund, versus 1/2% to own an index fund (where a fund manager only has to mimic an index, no decision making is required). Mutual funds are so diversified, you would be better off just buying an index fund. Most fund managers have too many stocks in their portfolios, anywhere from 50 to 200 or so. Look at the chart on page one of the Dow Jones Industrial Average versus the S&P 500 Index over the past two years. The lines are nearly identical, yet the Dow only has 30 stocks and the S&P has 500 – adding the additional 470 stocks to a portfolio would have actually hurt the performance.

What Really Happens when you Diversify

Though I picked two years for the chart on page one, almost any timeframe would show the Dow 30 outperforming the S&P 500 Index (even if just slightly). The reason this happens is that the Dow is comprised of the 30 highest quality industrial companies that represent (theoretically) the entire market. By limiting the index to 30 names, the Dow generally represents quality capital allocation opportunities. Compare this to the S&P 500, which does the same thing as the Dow, only it uses 500 companies. Clearly, if you have to make 500 capital allocation decisions, each successive decision will be worse than the prior decision.

That is the problem with over-diversification, every additional asset allocation decision you make is by definition weaker than the previous investment. So what are you left with when you over-diversify? At best average performance, and at worst massive under performance due to the excessive fees you incur buying and selling so many stocks (or funds).

Your performance will be average at best, because you have essentially diversified away all your hard work and research. You have watered your portfolio down with lower quality stocks. You are left with stock market risk not company specific risk, just the opposite of what you want. If the market goes down, your 30 companies will go down, if the market goes up, your 30 companies will go up. By over-diversifying you are leaving your portfolio at the mercy of the markets. Most financial professionals would have you believe this is a wise decision, I am telling you it is not.

Why do all the Research if you are Going to Diversify

As many of you know, I do not believe in a diversified portfolio. At Perpetual Value I can hold a maximum of ten positions, and I have no problem owning as few as four companies. I think the fund’s concentrated portfolio is its biggest selling point. Most investors simply do not have access to a similar product. You may be able to go to a broker and structure a concentrated portfolio, but you can rest assured the broker’s fee will not be contingent on whether or not you make money. The broker gets paid either way. In addition, any mutual fund you buy will have considerably more than 10 positions. The Perpetual Value fund is unique in that I am not scared to run a concentrated portfolio.

I believe that the whole point of portfolio management is to identify above average companies in which to invest. Finding such companies at reasonable prices is nearly impossible. It happens a handful of times a year if we are lucky. That is why the fund is so inactive, patience is a key component of our investment discipline.

Over-diversification is yet another way the financial industry has failed the investing public. It is far better to buy a handful of quality companies than many mediocre companies.

No comments:

Post a Comment