Keep it Simple

There is an interesting dynamic in the financial industry, complicated and seemingly ultra intelligent systems or investment strategies are thought of as superior to common sense. Frankly I don’t understand this reasoning, it is counterintuitive to lessons everyone learns early in life. Think about it, history is littered with so called sophisticated financial schemes. From the Hunt brothers trying to corner the silver market in 1973, to the mortgage securities derivative scandal of 1994, to the Nobel Laureate geniuses (or maybe more correctly not so bright geniuses) at Long Term Capital Management (LTCM) in 1998 – people have been trying to pitch sure fire, no risk complex systems.

Yet throughout time one thing remains certain, individuals complicating the simple process of financial analysis always come out losers. Note I wrote the process is simple not the execution. Drawing the correct conclusions from essentially unlimited data (noise), is nearly an impossible skill to master. It separates the proverbial men from the boys.

At Perpetual Value I am often asked if I use ‘sophisticated’ strategies – like options and derivatives. Or further what my intellectual edge is, do I have better information than the other portfolio managers, or am I just smarter in certain industries? Unfortunately there is no way to honestly quantify such questions. What portfolio manager is going to say he is dumb? Plain and simple such questions are asked by investors because they want to know if the fund is sexy. Doing realistic research and trying to manage downside risk is not sexy enough for them. They seem to want to believe that their chosen portfolio managers have super, all knowing powers. They essentially want to think they have a sure thing, or at least something to talk about at cocktail parties. While I understand the impetus behind such questions, I believe they are 100% misguided and likely harmful to one’s net worth. There is a difference between a portfolio manager that has an investment strategy that consistently (adjusted for risk) outperforms the broad markets and one that simply has a complicated, computer back tested, and seemingly low risk strategy that will change the world.

The Smartest Minds in the Country

The best example of a sophisticated, untested (for all possibilities) strategy is the Long-Term Capital Management disaster. For those interested I highly recommend Roger Lowenstein’s - When Genius Failed - it is well worth the $15. LTCM was billed as the most complex hedge fund out there, it was once thought of as nearly risk free! LTCM was run by literally the smartest guys in the country. They were math and financial geniuses. You may have heard of the famous options pricing model – the Black-Scholes model – well no less than Mr. Scholes himself was a managing partner in LTCM. LTCM was beyond sophisticated, they were beyond complex – they were actually authoring the efficient market theories others would study in universities around the globe.

The only problem was, they looked at investing like it was a pure science, like a few fundamental laws guided everything. Essentially, as the saying goes, they knew the price of everything (and its likely movements) but the VALUE of nothing. Their strategy weighed heavily on the historic price changes of securities – in essence all ‘complex’ systems rely on historic price movements. It’s funny that doesn’t seem so complex to me, it seems like circular logic, but not complex! See the LTCM guys, believing everything was a science and a mathematical probability, did not believe in the chaos theory. Their equations failed to take into account that historic correlation and liquidity could change based on new unforeseen events. You simply cannot model the chaos of global financial markets – the past won’t always predict the future.

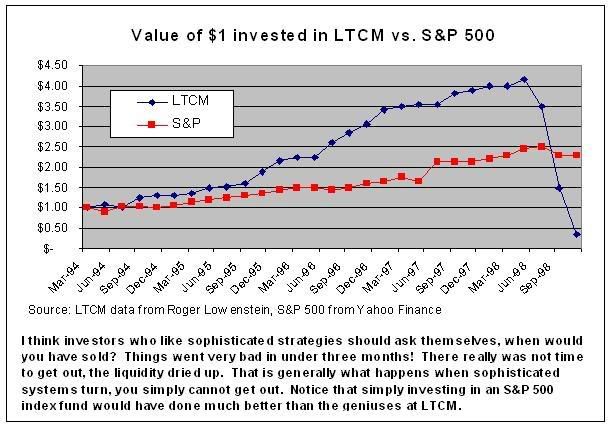

That is the biggest problem with so called sophisticated strategies, they all boil down to using historical results, from liquidity to operating margins, to predict exactly how a security will react

in the future. This is their big secret weapon, talk about a little man behind the curtain. Yet when the future doesn’t act exactly like their models suggest it should, sophisticated strategies tend to blow up magnificently. If you are not careful you lose all your money. See the chart on page one – it happens almost overnight!

It is important for investors to understand that instruments or strategies they perceive as sophisticated such as derivatives and options – are just mathematical formulas based on historical behavior and correlation. The same can be said for complex interest rate spread trading schemes – like LTCM employed – if the future is different then predicted everything falls to pieces. Some managers try to sell you complex black box strategies to make you think they are lowering risk and increasing returns. History shows the exact opposite is true, invariable these strategies are extremely risky.

Another trait most complex portfolio management strategies have is they use leverage – meaning you borrow money to try and enhance your returns. Again there is nothing too complex about borrowing money - any fool can do it. Yet the only thing you are really doing is increasing your risks proportionately to your increased return expectations. Really anyone can understand this, but it never fails, hedge funds that pitch very complex strategies generate a huge buzz and get people interested.

Buzz Isn’t Legal Tender

I am not interested in creating a buzz around Perpetual Value. I am more concerned with attracting investors that believe in our strategy. Investors that are smart enough to understand everything else is just dangerous financial engineering. Perpetual Value employs the most sophisticated strategy known: We think, we make judgements and we have conviction. I challenge other managers to come up with anything more complicated. Thinking is the hardest thing humans do. It’s what separates us from computers. Anyone with a $500 Dell computer can trade bond spreads and make interest rate bets or gamble with short-term put/call strategies. Yet only a select few portfolio managers have the patience to think and analyze.

Can Google really continue its rapid growth, while increasing profits in the face of fierce competition? Can mortgage originators, that have enjoyed years of the lowest interest rates EVER, really go up as interest rates move against them? Can a 106 year old children’s clothing company, with a history of returning over 15% on its invested capital, continue to trade at just 50% of depressed revenues? I am not really sure what a computer would say about those questions, but in my opinion I would say the answer is no. The ability to use logical reasoning is what really separates the best portfolio managers from the worst.

Remember the Great Ones

Think about legendary investors like Peter Lynch, Warren Buffett or John Templeton, all great independent thinkers. Now compare them to John Meriwether (of LTCM fame), junk bond king Michael Milken (his recent philanthropic work aside) or the rogue commodities trader Nick Leeson – they all at one point made hundreds of millions of dollars with their strategies. Yet the only reason anyone knows their names is because their ‘systems’ ultimately failed. Today nobody respects their investment views like the great thinkers previously mentioned.

Over the past 20 months that I have run the fund, the hardest concept to make investors understand is that Perpetual Value’s edge is its investment philosophy and strategy. Just because I don’t try and wow investors with seemingly complex discussions does not mean the fund is somehow unsophisticated, or worse that anyone could generate the same results. The core concepts of free cash flow, return on invested capital, normalized results and price sensitivity are not easy to properly execute. The investment process requires thinking, and most portfolio managers don’t think for themselves or they spend too much time focusing on the wrong things. They focus on the weekly news flow from a company, or they focus on some tiny piece of information that they incorrectly extrapolate into having some greater meaning. The ability to see the forest through the trees is often underestimated.

To date I am very pleased with how Perpetual Value’s investment strategy has performed in a relatively difficult market environment. Anyone can generate decent returns in a bull market, but it is much harder in a flat or down market. I am confident the core principles that comprise Perpetual Value’s strategy will never go out of style.

There is an interesting dynamic in the financial industry, complicated and seemingly ultra intelligent systems or investment strategies are thought of as superior to common sense. Frankly I don’t understand this reasoning, it is counterintuitive to lessons everyone learns early in life. Think about it, history is littered with so called sophisticated financial schemes. From the Hunt brothers trying to corner the silver market in 1973, to the mortgage securities derivative scandal of 1994, to the Nobel Laureate geniuses (or maybe more correctly not so bright geniuses) at Long Term Capital Management (LTCM) in 1998 – people have been trying to pitch sure fire, no risk complex systems.

Yet throughout time one thing remains certain, individuals complicating the simple process of financial analysis always come out losers. Note I wrote the process is simple not the execution. Drawing the correct conclusions from essentially unlimited data (noise), is nearly an impossible skill to master. It separates the proverbial men from the boys.

At Perpetual Value I am often asked if I use ‘sophisticated’ strategies – like options and derivatives. Or further what my intellectual edge is, do I have better information than the other portfolio managers, or am I just smarter in certain industries? Unfortunately there is no way to honestly quantify such questions. What portfolio manager is going to say he is dumb? Plain and simple such questions are asked by investors because they want to know if the fund is sexy. Doing realistic research and trying to manage downside risk is not sexy enough for them. They seem to want to believe that their chosen portfolio managers have super, all knowing powers. They essentially want to think they have a sure thing, or at least something to talk about at cocktail parties. While I understand the impetus behind such questions, I believe they are 100% misguided and likely harmful to one’s net worth. There is a difference between a portfolio manager that has an investment strategy that consistently (adjusted for risk) outperforms the broad markets and one that simply has a complicated, computer back tested, and seemingly low risk strategy that will change the world.

The Smartest Minds in the Country

The best example of a sophisticated, untested (for all possibilities) strategy is the Long-Term Capital Management disaster. For those interested I highly recommend Roger Lowenstein’s - When Genius Failed - it is well worth the $15. LTCM was billed as the most complex hedge fund out there, it was once thought of as nearly risk free! LTCM was run by literally the smartest guys in the country. They were math and financial geniuses. You may have heard of the famous options pricing model – the Black-Scholes model – well no less than Mr. Scholes himself was a managing partner in LTCM. LTCM was beyond sophisticated, they were beyond complex – they were actually authoring the efficient market theories others would study in universities around the globe.

The only problem was, they looked at investing like it was a pure science, like a few fundamental laws guided everything. Essentially, as the saying goes, they knew the price of everything (and its likely movements) but the VALUE of nothing. Their strategy weighed heavily on the historic price changes of securities – in essence all ‘complex’ systems rely on historic price movements. It’s funny that doesn’t seem so complex to me, it seems like circular logic, but not complex! See the LTCM guys, believing everything was a science and a mathematical probability, did not believe in the chaos theory. Their equations failed to take into account that historic correlation and liquidity could change based on new unforeseen events. You simply cannot model the chaos of global financial markets – the past won’t always predict the future.

That is the biggest problem with so called sophisticated strategies, they all boil down to using historical results, from liquidity to operating margins, to predict exactly how a security will react

in the future. This is their big secret weapon, talk about a little man behind the curtain. Yet when the future doesn’t act exactly like their models suggest it should, sophisticated strategies tend to blow up magnificently. If you are not careful you lose all your money. See the chart on page one – it happens almost overnight!

It is important for investors to understand that instruments or strategies they perceive as sophisticated such as derivatives and options – are just mathematical formulas based on historical behavior and correlation. The same can be said for complex interest rate spread trading schemes – like LTCM employed – if the future is different then predicted everything falls to pieces. Some managers try to sell you complex black box strategies to make you think they are lowering risk and increasing returns. History shows the exact opposite is true, invariable these strategies are extremely risky.

Another trait most complex portfolio management strategies have is they use leverage – meaning you borrow money to try and enhance your returns. Again there is nothing too complex about borrowing money - any fool can do it. Yet the only thing you are really doing is increasing your risks proportionately to your increased return expectations. Really anyone can understand this, but it never fails, hedge funds that pitch very complex strategies generate a huge buzz and get people interested.

Buzz Isn’t Legal Tender

I am not interested in creating a buzz around Perpetual Value. I am more concerned with attracting investors that believe in our strategy. Investors that are smart enough to understand everything else is just dangerous financial engineering. Perpetual Value employs the most sophisticated strategy known: We think, we make judgements and we have conviction. I challenge other managers to come up with anything more complicated. Thinking is the hardest thing humans do. It’s what separates us from computers. Anyone with a $500 Dell computer can trade bond spreads and make interest rate bets or gamble with short-term put/call strategies. Yet only a select few portfolio managers have the patience to think and analyze.

Can Google really continue its rapid growth, while increasing profits in the face of fierce competition? Can mortgage originators, that have enjoyed years of the lowest interest rates EVER, really go up as interest rates move against them? Can a 106 year old children’s clothing company, with a history of returning over 15% on its invested capital, continue to trade at just 50% of depressed revenues? I am not really sure what a computer would say about those questions, but in my opinion I would say the answer is no. The ability to use logical reasoning is what really separates the best portfolio managers from the worst.

Remember the Great Ones

Think about legendary investors like Peter Lynch, Warren Buffett or John Templeton, all great independent thinkers. Now compare them to John Meriwether (of LTCM fame), junk bond king Michael Milken (his recent philanthropic work aside) or the rogue commodities trader Nick Leeson – they all at one point made hundreds of millions of dollars with their strategies. Yet the only reason anyone knows their names is because their ‘systems’ ultimately failed. Today nobody respects their investment views like the great thinkers previously mentioned.

Over the past 20 months that I have run the fund, the hardest concept to make investors understand is that Perpetual Value’s edge is its investment philosophy and strategy. Just because I don’t try and wow investors with seemingly complex discussions does not mean the fund is somehow unsophisticated, or worse that anyone could generate the same results. The core concepts of free cash flow, return on invested capital, normalized results and price sensitivity are not easy to properly execute. The investment process requires thinking, and most portfolio managers don’t think for themselves or they spend too much time focusing on the wrong things. They focus on the weekly news flow from a company, or they focus on some tiny piece of information that they incorrectly extrapolate into having some greater meaning. The ability to see the forest through the trees is often underestimated.

To date I am very pleased with how Perpetual Value’s investment strategy has performed in a relatively difficult market environment. Anyone can generate decent returns in a bull market, but it is much harder in a flat or down market. I am confident the core principles that comprise Perpetual Value’s strategy will never go out of style.

No comments:

Post a Comment